Cross-border payment refers to the currency receipt and payment behavior arising from international trade, investment, or personal fund transfer between two or more countries or regions. The common cross-border payment methods are as follows:

Traditional Financial Institution Payment Methods

They are the most fundamental and commonly used means of cross-border payment, leveraging the global networks of traditional financial institutions like banks to handle fund settlement.

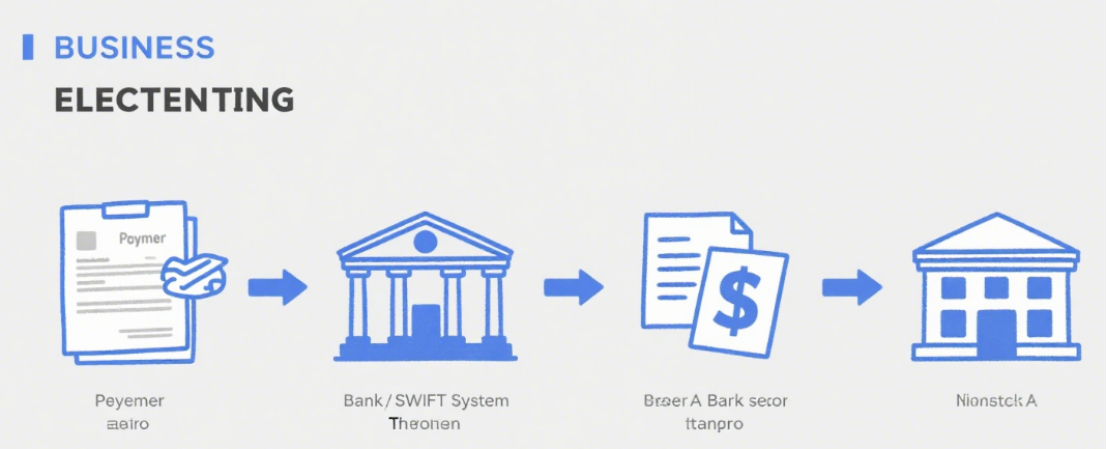

Telegraphic Transfer (T/T)

Principle: Transfer funds from the payer’s bank account to the payee’s bank account via interbank electronic communication systems (e.g., SWIFT).

Characteristics: High security and relatively stable arrival time (usually 1-5 business days). However, the fees are high, covering remitting bank fees, intermediary bank fees, receiving bank fees, etc. Besides, exchange rates may fluctuate.

Applicable Scenarios: Large-scale trade settlements, inter-enterprise fund transfers, tuition payments for studying abroad, etc.

Letter of Credit (L/C)

Principle: A conditional payment commitment issued by a bank to an exporter at the request of an importer. The bank will pay as long as the exporter submits documents compliant with L/C requirements.

Characteristics: It’s secured by bank credit, reducing buyers’ and sellers’ credit risks. Yet, it involves complex procedures and high costs, including opening, amendment, and notification fees, and its processing cycle is long.

Applicable Scenarios: International trade transactions with large amounts and mutual distrust between buyers and sellers, particularly for first-time cooperations.

Collection

Principle: The exporter entrusts a bank to collect payment from the importer, divided into clean collection and documentary collection. In documentary collection, the exporter gives drafts together with commercial documents (e.g., bills of lading, invoices) to the bank for collection.

Characteristics: Lower fees and simpler procedures than L/C. But the risk is higher, since the importer might refuse payment or acceptance. The bank just transfers documents and collects payment without bearing payment liability.

Applicable Scenarios: International trade settlements where both parties have a cooperation basis and know each other’s credit to some extent.

Third-Party Payment Platform Payment Methods

With internet development, third-party payment platforms are widely used in cross-border payments for convenience and efficiency.

Internationally Renowned Third-Party Payment Platforms

PayPal: One of the world’s most extensively used platforms, supporting multi-currency transactions. Users can make cross-border payments after registering and linking a bank card or credit card. It is convenient and secure, but costly, with transaction and currency conversion fees, and has usage limitations in some areas.

Stripe: Focused on corporate clients, offering online payment solutions and supporting multiple means like credit and debit cards. It features strong integration, suiting e-commerce websites and SaaS platforms. Its fees are transparent and arrival time is fast, but its merchant review is strict.

Chinese Third-Party Payment Platforms (Supporting Cross-Border Services)

Alipay: In cross-border payments, it allows users to spend at overseas offline merchants and shop online. Via cooperation with local institutions, it converts RMB to local currencies. It is user-friendly for Chinese, convenient, and offers favorable exchange rates and promotions.

WeChat Pay: Similar to Alipay, it’s commonly used in overseas Chinese communities and eligible merchants. It enables QR code payment and money transfer, being convenient and favored by Chinese users.

Other Cross-Border Payment Methods

Debit/Credit Card Payment

Principle: When using international cards (e.g., Visa, Mastercard, UnionPay) for overseas consumption or online shopping, payments are made directly. Banks convert amounts by exchange rates and settle accounts.

Characteristics: High convenience, no need to exchange foreign currency in advance. But it may incur cross-border and currency conversion fees, and there’s a risk of card fraud.

Applicable Scenarios: Small payments like overseas travel expenses and cross-border online shopping.

Digital Currency Payment

Principle: Utilize digital currencies like Bitcoin and Ethereum for cross-border transfers via blockchain, without relying on banks.

Characteristics: Fast transactions, low fees for some currencies, and strong anonymity. However, it has huge price volatility, ambiguous regulations, and high legal and market risks.

Applicable Scenarios: Currently used in niche cross-border transactions, not yet a mainstream method.

Post time: Aug-21-2025